All Categories

Featured

Table of Contents

The are entire life insurance coverage and global life insurance policy. The money worth is not included to the fatality advantage.

After ten years, the cash value has actually grown to about $150,000. He takes out a tax-free car loan of $50,000 to start a company with his bro. The plan car loan rates of interest is 6%. He repays the financing over the following 5 years. Going this route, the interest he pays goes back into his policy's money value as opposed to a banks.

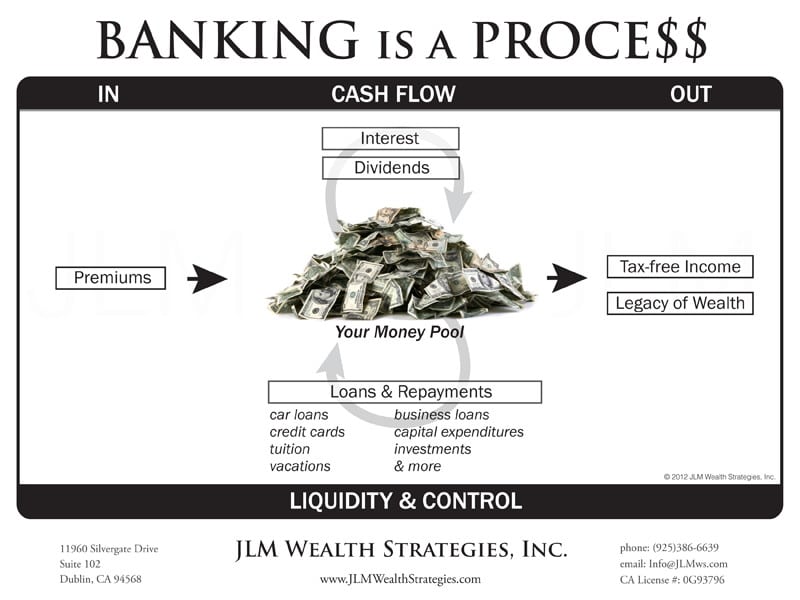

Infinite Banking Life Insurance

The idea of Infinite Banking was produced by Nelson Nash in the 1980s. Nash was a money specialist and fan of the Austrian institution of economics, which advocates that the value of products aren't clearly the outcome of typical economic structures like supply and need. Instead, people value cash and products in different ways based upon their economic standing and requirements.

One of the pitfalls of standard banking, according to Nash, was high-interest prices on finances. Long as banks established the rate of interest rates and financing terms, individuals didn't have control over their very own riches.

Infinite Financial needs you to own your economic future. For ambitious people, it can be the finest financial device ever. Right here are the advantages of Infinite Banking: Perhaps the single most advantageous aspect of Infinite Financial is that it enhances your cash circulation.

Dividend-paying whole life insurance policy is very low threat and supplies you, the policyholder, a good deal of control. The control that Infinite Financial provides can best be grouped right into 2 classifications: tax advantages and possession defenses - is infinite banking a scam. Among the factors entire life insurance policy is optimal for Infinite Banking is just how it's exhausted.

Nelson Nash Infinite Banking

When you make use of whole life insurance for Infinite Financial, you enter right into a personal contract between you and your insurance coverage company. These defenses might vary from state to state, they can include protection from possession searches and seizures, security from judgements and protection from lenders.

Whole life insurance policy policies are non-correlated assets. This is why they function so well as the economic foundation of Infinite Financial. Regardless of what happens in the market (supply, actual estate, or otherwise), your insurance coverage policy maintains its well worth.

Entire life insurance coverage is that third pail. Not only is the price of return on your whole life insurance coverage plan ensured, your fatality advantage and costs are likewise guaranteed.

This structure aligns completely with the concepts of the Perpetual Wealth Strategy. Infinite Banking attract those looking for higher monetary control. Right here are its major advantages: Liquidity and access: Policy fundings provide immediate accessibility to funds without the limitations of conventional small business loan. Tax effectiveness: The cash value grows tax-deferred, and plan loans are tax-free, making it a tax-efficient device for constructing wealth.

Infinite Banking Policy

Property security: In many states, the money worth of life insurance policy is shielded from creditors, including an added layer of financial safety. While Infinite Banking has its advantages, it isn't a one-size-fits-all remedy, and it comes with considerable disadvantages. Right here's why it may not be the very best approach: Infinite Financial commonly requires intricate plan structuring, which can confuse policyholders.

Think of never having to fret about small business loan or high rates of interest again. Suppose you could borrow money on your terms and construct wealth all at once? That's the power of unlimited financial life insurance. By leveraging the money worth of whole life insurance coverage IUL policies, you can expand your riches and obtain money without relying on standard financial institutions.

There's no collection finance term, and you have the freedom to select the repayment timetable, which can be as leisurely as paying off the lending at the time of death. This versatility reaches the servicing of the loans, where you can select interest-only payments, maintaining the car loan equilibrium flat and convenient.

Holding cash in an IUL repaired account being attributed passion can usually be far better than holding the cash money on deposit at a bank.: You have actually constantly desired for opening your very own pastry shop. You can borrow from your IUL policy to cover the first expenses of renting out an area, acquiring equipment, and employing personnel.

Bank Concept

Individual lendings can be obtained from traditional banks and lending institution. Here are some vital factors to take into consideration. Bank card can offer an adaptable way to obtain money for really temporary durations. Obtaining cash on a credit report card is generally extremely expensive with yearly percentage prices of interest (APR) usually getting to 20% to 30% or more a year.

The tax obligation treatment of plan car loans can differ considerably relying on your country of house and the particular regards to your IUL policy. In some regions, such as The United States and Canada, the United Arab Emirates, and Saudi Arabia, plan car loans are typically tax-free, using a significant benefit. In other territories, there may be tax ramifications to think about, such as prospective tax obligations on the car loan.

Term life insurance policy only provides a survivor benefit, without any type of cash money value buildup. This indicates there's no cash money value to obtain against. This article is authored by Carlton Crabbe, President of Capital permanently, an expert in supplying indexed global life insurance policy accounts. The information provided in this write-up is for academic and informational objectives only and need to not be understood as financial or financial investment suggestions.

For lending officers, the considerable regulations imposed by the CFPB can be seen as difficult and restrictive. Car loan police officers often argue that the CFPB's guidelines create unnecessary red tape, leading to even more documents and slower loan processing. Rules like the TILA-RESPA Integrated Disclosure (TRID) regulation and the Ability-to-Repay (ATR) needs, while focused on protecting customers, can lead to hold-ups in closing bargains and raised operational costs.

{kind=link}

Latest Posts

Infinite Banking Insurance

Be Your Own Bank With The Infinite Banking Concept

Life Insurance Banking